Why the Middle of the Yield Curve Is Gaining Attention Globally and What Indian Investors Should Know

Fixed income investors are facing an unusual challenge in 2026.

Cash and short-term debt continue to offer attractive yields, while long-duration bonds remain vulnerable to changing inflation expectations and uncertain interest-rate paths. In this environment, investors are increasingly asking a simple question:

Where should capital be positioned on the yield curve today?

Increasingly, global asset managers believe the answer lies in the middle of the yield curve also known as the “belly of the curve” represented by 5-year bonds and other intermediate-duration bonds.

From BlackRock and PGIM to UBS Chief Investment Office, institutional investors are highlighting this segment as a potential sweet spot for income generation, portfolio stability, and attractive risk-adjusted returns.

For Indian investors, this trend matters because many of the same principles driving global bond allocations can also influence positioning within Indian government securities, target maturity funds, and debt portfolios.

Why This Theme Is Gaining Attention in 2026

Several macroeconomic forces are driving renewed interest in the middle of the yield curve:

- Inflation remains above many central bank targets.

- Rate-cut expectations continue to shift.

- Investors are prioritizing income rather than making aggressive duration bets.

- Bond yields remain attractive relative to the post-2010 period.

- Institutional investors are focusing on efficient risk-adjusted returns.

As a result, many portfolio managers are favoring intermediate-duration bonds over both very short and very long maturities.

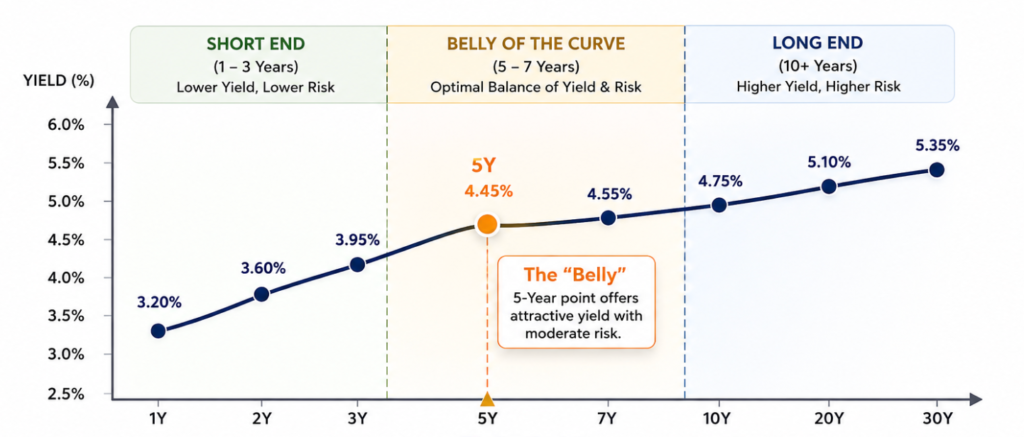

What Is the “Belly” of the Yield Curve?

Featured Definition

The belly of the yield curve refers to bonds with maturities between five and seven years. These intermediate-duration bonds sit between short-term and long-term debt securities and are often considered a balance between income generation and interest-rate risk.

A typical yield curve can be divided into three segments:

- Short-term bonds: 1–3 years

- Middle curve (“belly”): 5–7 years

- Long-term bonds: 10–30 years

While investors often focus on headline-grabbing 10-year bond yields, the middle segment is increasingly viewed as the most attractive area of the curve.

Why the Middle of the Yield Curve Is Becoming the Sweet Spot

1. Attractive Income Through Positive Carry

One of the biggest advantages of intermediate-duration bonds is positive carry the income investors earn simply by holding the bond.

In today’s environment, investors can lock in attractive yields without taking excessive duration risk.

BlackRock’s fixed income team has repeatedly emphasized that income and carry have become major drivers of total return as bond yields remain elevated compared to the previous decade.

2. Roll-Down Benefit Can Enhance Returns

A lesser-known advantage is the roll-down benefit.

As bonds age, they move down the yield curve toward shorter maturities. If shorter maturities trade at lower yields, bond prices can appreciate even without changes in interest rates.

For example:

- A 5-year bond becomes a 4-year bond.

- A 4-year bond often trades at a lower yield.

- Lower yields generally mean higher bond prices.

This creates an additional return source beyond coupon income.

3. Lower Volatility Than Long-Term Bonds

While long-duration bonds may offer capital appreciation potential when rates fall, they are significantly more sensitive to interest-rate movements.

The middle curve provides:

- Lower duration risk

- More stable returns

- Reduced drawdowns

- Better portfolio resilience

UBS CIO has highlighted quality government bonds in short-to-medium maturities as attractive opportunities for investors seeking stability alongside income.

4. Better Yield Potential Than Cash

Short-term instruments remain useful for liquidity management, but they expose investors to reinvestment risk.

If rates decline, investors may need to reinvest at lower yields.

Intermediate maturities allow investors to lock in current yields for longer periods while avoiding the volatility of long-duration bonds.

What the Data Is Showing

Recent market performance supports the institutional preference for the belly of the curve.

According to Bloomberg Treasury indexes cited by market participants, the 5–7-year Treasury segment generated approximately 7% returns, outperforming the broader bond market’s gain of around 5.4%.

This performance reflects a combination of:

- Attractive carry

- Roll-down returns

- Moderate duration exposure

- Improved risk-adjusted outcomes

For many portfolio managers, this reinforces the view that the middle curve currently offers one of the most compelling opportunities in global fixed income.

Comparing Different Parts of the Yield Curve

| Factor | Short End (1–3 Years) | Middle Curve (5–7 Years) | Long End (10+ Years) |

| Yield Potential | Moderate | High | High |

| Interest Rate Sensitivity | Low | Moderate | High |

| Volatility | Low | Moderate | High |

| Positive Carry | Limited | Strong | Strong |

| Roll-Down Benefit | Limited | Attractive | Moderate |

| Portfolio Stability | High | High | Lower |

| Institutional Preference (2026) | Neutral | Strong | Selective |

Portfolio Strategist Insight

When uncertainty around interest rates remains elevated, investors often face a trade-off between maximizing yield and preserving capital. The middle of the yield curve can help bridge that gap by offering attractive income opportunities while avoiding the heightened volatility associated with long-duration bonds.

What This Means for Indian Debt Investors

The global focus on the middle of the yield curve has important implications for Indian investors.

Indian government securities continue to offer attractive yields compared to many developed markets, with the 10-year G-Sec remaining near the 7% range through much of 2025–2026.

However, the opportunity is not simply about chasing yield.

It is about identifying where the best risk-adjusted opportunities exist across maturities.

For Retail Investors

Investors exploring a fixed income strategy for 2026 in India may consider:

- Target Maturity Funds

- Corporate Bond Funds

- Banking & PSU Debt Funds

- RBI Floating Rate Savings Bonds

These products can provide diversified exposure while benefiting from intermediate-duration positioning.

For HNI Investors

HNIs may evaluate:

- Direct Government Securities (G-Secs)

- State Development Loans (SDLs)

- High-quality Corporate Bonds

- Fixed Income PMS Strategies

- Laddered Bond Portfolios

These approaches can help balance income generation with duration management.

RBI Policy Could Become a Key Catalyst for bond market performance

The future path of RBI policy remains one of the most important variables for Indian fixed income markets.

If rate cuts emerge during the next policy cycle:

- Intermediate-duration bonds could benefit from price appreciation.

- Investors could capture coupon income plus capital gains.

- Portfolio volatility may remain lower than long-duration alternatives.

For investors evaluating intermediate-duration debt funds in India, the current environment may present a compelling opportunity to reassess portfolio positioning.

How Investors Can Position Fixed Income Portfolios

Rather than making concentrated bets, many strategists advocate a diversified approach.

A balanced portfolio may include:

Liquidity Allocation

- Money market funds

- Ultra-short duration funds

- Cash reserves

Core Income Allocation

- Intermediate-duration debt funds

- Target maturity funds

- Government securities

Tactical Allocation

- Select long-duration opportunities

- Duration positioning based on policy outlook

The objective is not simply maximizing yield.

The objective is maximizing risk-adjusted returns.

Conclusion

The growing institutional focus on the middle of the yield curve reflects a broader shift in how investors are approaching fixed income in 2026.

The 5-year segment offers a compelling combination of:

- Positive carry

- Roll-down benefit

- Higher yields than short-term instruments

- Lower volatility than long-duration bonds

For Indian investors navigating changing interest-rate expectations and evolving RBI policy, the middle of the curve may represent one of the most attractive opportunities in today’s debt markets.

Frequently Asked Questions

What is the middle of the yield curve?

The middle of the yield curve refers to bonds with maturities between five and seven years, often called the belly of the curve.

Why are investors buying 5-year bonds?

Many investors view 5-year bonds as offering an attractive balance between income generation, capital preservation, and duration risk.

What is positive carry?

Positive carry is the income earned by holding a bond, primarily through coupon payments and yield accrual.

What is a roll-down benefit?

Roll-down occurs when a bond moves closer to maturity and benefits from the lower yields associated with shorter-duration securities.

Are intermediate-duration bonds safer than long-term bonds?

Generally, they experience lower price volatility and reduced interest-rate sensitivity compared with long-term bonds.

How can Indian investors gain exposure to this strategy?

Through target maturity funds, debt mutual funds, government securities, corporate bonds, and professionally managed fixed income portfolios.