For many investors, the search for higher returns often begins with one question:

Which investment pays the highest yield?

But experienced investors tend to ask a different question:

How much of that return will I actually keep?

In fixed income investing, a higher headline yield does not automatically translate into better outcomes. Taxes, credit risk, liquidity constraints, and portfolio structure all influence what ultimately reaches an investor’s pocket.

As we move through 2026, interest rates remain relatively attractive compared to recent years, creating opportunities for investors seeking income and stability. At the same time, market uncertainty, evolving tax considerations, and changing liquidity needs make investment selection more important than ever.

For both retail investors and HNIs, the objective should not simply be generating income. It should be finding ways to preserve capital and optimise post-tax yield while maintaining flexibility and managing risk appropriately.

A disciplined fixed income strategy can help achieve exactly that.

Looking Beyond Headline Returns

One of the most common mistakes investors make is evaluating investments solely on the basis of advertised returns.

Consider two fixed income opportunities:

Investment A offers 8.0%

Investment B offers 7.2%

Most investors instinctively gravitate toward the higher number.

However, the higher-yielding investment may involve additional credit risk, lower liquidity, or tax consequences that reduce its actual attractiveness.

The most successful investors understand that investment returns should never be evaluated in isolation.

Instead, every investment should be assessed across three dimensions:

Risk

Liquidity

After-tax returns

When viewed through this broader lens, the investment with the highest stated yield is not always the most rewarding choice.

Why Capital Protection Matters More Than Chasing Yield

Building wealth and protecting wealth require different mindsets.

Early in an investor’s journey, the focus is often on growth. As wealth accumulates, avoiding unnecessary losses becomes increasingly important.

Recovering from significant capital losses can take years.

For example:

A portfolio that falls 20% requires a 25% gain to recover.

A portfolio that falls 30% requires nearly 43% growth to break even.

This simple reality explains why many sophisticated investors place risk management ahead of return maximisation.

Protecting principal provides the foundation that allows wealth to compound consistently over time.

That does not mean avoiding all risk.

It means ensuring that every risk taken is deliberate, understood, and appropriately compensated.

Why Post-Tax Yield Deserves More Attention

Many investors spend considerable effort comparing interest rates but devote far less attention to taxation.

Yet taxes can significantly influence investment outcomes.Post-tax yield represents the return that remains after applicable taxes have been paid.

This is often a more meaningful measure of success than pre-tax returns.

An Example for Indian Investors

Assume an investor in a higher tax bracket earns ₹10 lakh annually from fixed income investments.

A decision that improves after-tax returns by even 1% can translate into meaningful additional income over time.

More importantly, these improvements often come without increasing portfolio risk.

The result is a stronger long-term outcome achieved through better portfolio construction rather than greater risk-taking.

This is one reason tax-efficient investing has become an increasingly important consideration for both retail investors and HNIs.

The Three Pillars of a Fixed Income Strategy in 2026

Successful fixed income investing is rarely about selecting a single product.

Instead, it involves balancing three interconnected objectives.

Stability

Investors should prioritise high-quality investments that provide confidence in the repayment of principal.

Credit quality remains one of the most important factors in fixed income investing.

Higher yields may appear attractive, but they should always be evaluated alongside the risks required to achieve them.

Liquidity

Access to capital matters.

Unexpected opportunities, business requirements, education expenses, and personal financial needs can arise at any time.

Returns should be evaluated on a net basis rather than a gross basis.

A portfolio that generates slightly lower pre-tax returns but offers greater efficiency may ultimately create better investor outcomes.

Fixed Income Options Worth Considering in 2026

Different fixed income instruments serve different purposes.

Rather than searching for a single solution, investors should understand where each instrument fits within a broader portfolio.

Government Securities

Government securities remain among the highest-quality fixed income investments available to Indian investors.

Because they are backed by the Government of India, they are often used by investors seeking portfolio stability and capital protection.

They can serve as a strong foundation for conservative fixed income allocations.

Target Maturity Funds

Target maturity funds have become increasingly popular due to their transparency and defined maturity profiles.

These funds typically invest in government securities or high-quality bonds that mature around a predetermined date.

They may be particularly useful for investors planning around specific financial goals such as retirement, education funding, or large future expenses.

Corporate Bond Funds

Corporate bond funds can offer additional income potential while maintaining relatively high credit quality.

Investors should prioritise funds that focus on stronger issuers rather than those pursuing aggressive yield enhancement strategies.

The quality of the underlying portfolio matters far more than marginal differences in yield.

Short- and Intermediate-Duration Debt Funds

For investors seeking a balance between income generation and interest-rate sensitivity, short- and intermediate-duration debt funds may provide useful diversification.

These funds can help manage volatility while still offering competitive fixed income exposure.

Laddered Bond Portfolios

Bond ladders involve spreading investments across multiple maturity dates.

Rather than committing all capital to a single maturity, investors stagger maturities over time.

This approach may help reduce reinvestment risk, improve liquidity management, and create greater flexibility during changing interest-rate cycles.

Common Mistakes That Can Impact Investor Outcomes

Prioritising Yield Over Quality

A higher yield is only beneficial if investors ultimately receive both their income and principal.

Quality should always come before incremental return.

Ignoring Tax Implications

Investments should be evaluated based on what remains after taxes rather than on stated returns alone.

This simple shift in perspective often leads to better long-term decisions.

Taking Concentrated Credit Risk

Overexposure to a small number of issuers or sectors can increase portfolio vulnerability.

Diversification remains one of the most effective risk-management tools available to investors.

Holding Excessive Cash

Cash provides safety and liquidity, but excessive allocations can create a drag on long-term returns.

A balanced fixed income allocation may help investors maintain liquidity while putting capital to work more efficiently.

Neglecting Portfolio Reviews

Interest rates, market conditions, and personal financial circumstances change over time.

Regular reviews help ensure portfolios remain aligned with investor objectives.

Frequently Asked Questions

What does it mean to preserve capital?

Preserving capital means protecting the original investment amount from significant losses while generating reasonable returns.

Why is post-tax yield important?

Post-tax yield reflects the return investors actually retain after taxes, making it a more meaningful measure than headline yield alone.

What is tax-efficient investing?

Tax-efficient investing involves structuring investments in a way that seeks to maximise after-tax returns without taking unnecessary risks.

Are government securities suitable for conservative investors?

Government securities are generally considered among the safest fixed income investments available because they are backed by the Government of India.

What is a good fixed income strategy for 2026?

A diversified approach that balances quality, liquidity, tax efficiency, and income generation can help investors navigate changing market conditions more effectively.

Closing Takeaway

In 2026, fixed income investing is about far more than simply earning interest.

The most effective portfolios balance quality, liquidity, diversification, and tax efficiency while remaining aligned with long-term financial objectives.

Investors who focus on preserving wealth, improving after-tax outcomes, and managing risk thoughtfully are often better positioned to navigate changing market environments with confidence.

A disciplined approach may not always generate the highest headline return, but it can help create something far more valuable: consistency.

Fixed income investors are facing an unusual challenge in 2026.

Cash and short-term debt continue to offer attractive yields, while long-duration bonds remain vulnerable to changing inflation expectations and uncertain interest-rate paths. In this environment, investors are increasingly asking a simple question:

Where should capital be positioned on the yield curve today?

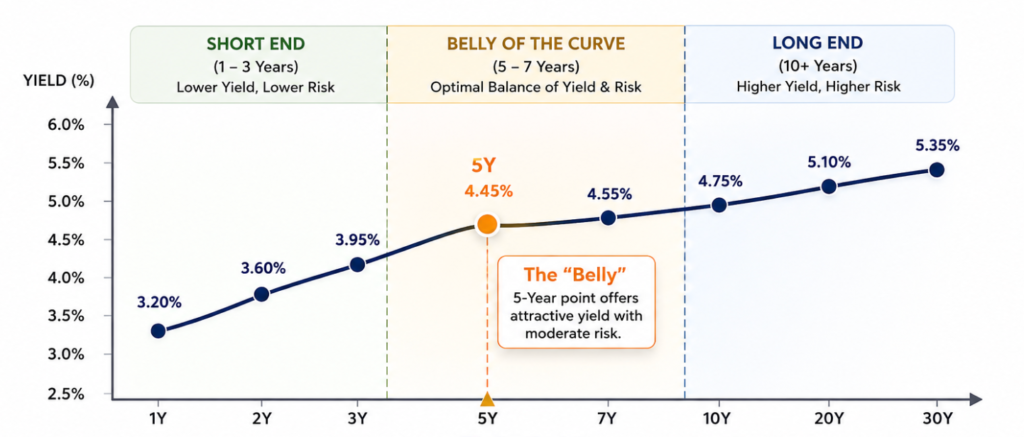

Increasingly, global asset managers believe the answer lies in the middle of the yield curve also known as the “belly of the curve” represented by 5-year bonds and other intermediate-duration bonds.

From BlackRock and PGIM to UBS Chief Investment Office, institutional investors are highlighting this segment as a potential sweet spot for income generation, portfolio stability, and attractive risk-adjusted returns.

For Indian investors, this trend matters because many of the same principles driving global bond allocations can also influence positioning within Indian government securities, target maturity funds, and debt portfolios.

Why This Theme Is Gaining Attention in 2026

Several macroeconomic forces are driving renewed interest in the middle of the yield curve:

Inflation remains above many central bank targets.

Rate-cut expectations continue to shift.

Investors are prioritizing income rather than making aggressive duration bets.

Bond yields remain attractive relative to the post-2010 period.

Institutional investors are focusing on efficient risk-adjusted returns.

As a result, many portfolio managers are favoring intermediate-duration bonds over both very short and very long maturities.

What Is the “Belly” of the Yield Curve?

Featured Definition

The belly of the yield curve refers to bonds with maturities between five and seven years. These intermediate-duration bonds sit between short-term and long-term debt securities and are often considered a balance between income generation and interest-rate risk.

A typical yield curve can be divided into three segments:

Short-term bonds: 1–3 years

Middle curve (“belly”): 5–7 years

Long-term bonds: 10–30 years

While investors often focus on headline-grabbing 10-year bond yields, the middle segment is increasingly viewed as the most attractive area of the curve.

Why the Middle of the Yield Curve Is Becoming the Sweet Spot

1. Attractive Income Through Positive Carry

One of the biggest advantages of intermediate-duration bonds is positive carry the income investors earn simply by holding the bond.

In today’s environment, investors can lock in attractive yields without taking excessive duration risk.

BlackRock’s fixed income team has repeatedly emphasized that income and carry have become major drivers of total return as bond yields remain elevated compared to the previous decade.

2. Roll-Down Benefit Can Enhance Returns

A lesser-known advantage is the roll-down benefit.

As bonds age, they move down the yield curve toward shorter maturities. If shorter maturities trade at lower yields, bond prices can appreciate even without changes in interest rates.

For example:

A 5-year bond becomes a 4-year bond.

A 4-year bond often trades at a lower yield.

Lower yields generally mean higher bond prices.

This creates an additional return source beyond coupon income.

3. Lower Volatility Than Long-Term Bonds

While long-duration bonds may offer capital appreciation potential when rates fall, they are significantly more sensitive to interest-rate movements.

The middle curve provides:

Lower duration risk

More stable returns

Reduced drawdowns

Better portfolio resilience

UBS CIO has highlighted quality government bonds in short-to-medium maturities as attractive opportunities for investors seeking stability alongside income.

4. Better Yield Potential Than Cash

Short-term instruments remain useful for liquidity management, but they expose investors to reinvestment risk.

If rates decline, investors may need to reinvest at lower yields.

Intermediate maturities allow investors to lock in current yields for longer periods while avoiding the volatility of long-duration bonds.

What the Data Is Showing

Recent market performance supports the institutional preference for the belly of the curve.

According to Bloomberg Treasury indexes cited by market participants, the 5–7-year Treasury segment generated approximately 7% returns, outperforming the broader bond market’s gain of around 5.4%.

This performance reflects a combination of:

Attractive carry

Roll-down returns

Moderate duration exposure

Improved risk-adjusted outcomes

For many portfolio managers, this reinforces the view that the middle curve currently offers one of the most compelling opportunities in global fixed income.

Comparing Different Parts of the Yield Curve

Factor

Short End (1–3 Years)

Middle Curve (5–7 Years)

Long End (10+ Years)

Yield Potential

Moderate

High

High

Interest Rate Sensitivity

Low

Moderate

High

Volatility

Low

Moderate

High

Positive Carry

Limited

Strong

Strong

Roll-Down Benefit

Limited

Attractive

Moderate

Portfolio Stability

High

High

Lower

Institutional Preference (2026)

Neutral

Strong

Selective

Portfolio Strategist Insight

When uncertainty around interest rates remains elevated, investors often face a trade-off between maximizing yield and preserving capital. The middle of the yield curve can help bridge that gap by offering attractive income opportunities while avoiding the heightened volatility associated with long-duration bonds.

What This Means for Indian Debt Investors

The global focus on the middle of the yield curve has important implications for Indian investors.

Indian government securities continue to offer attractive yields compared to many developed markets, with the 10-year G-Sec remaining near the 7% range through much of 2025–2026.

However, the opportunity is not simply about chasing yield.

It is about identifying where the best risk-adjusted opportunities exist across maturities.

For Retail Investors

Investors exploring a fixed income strategy for 2026 in India may consider:

Target Maturity Funds

Corporate Bond Funds

Banking & PSU Debt Funds

RBI Floating Rate Savings Bonds

These products can provide diversified exposure while benefiting from intermediate-duration positioning.

For HNI Investors

HNIs may evaluate:

Direct Government Securities (G-Secs)

State Development Loans (SDLs)

High-quality Corporate Bonds

Fixed Income PMS Strategies

Laddered Bond Portfolios

These approaches can help balance income generation with duration management.

RBI Policy Could Become a Key Catalyst for bond market performance

The future path of RBI policy remains one of the most important variables for Indian fixed income markets.

If rate cuts emerge during the next policy cycle:

Intermediate-duration bonds could benefit from price appreciation.

Investors could capture coupon income plus capital gains.

Portfolio volatility may remain lower than long-duration alternatives.

For investors evaluating intermediate-duration debt funds in India, the current environment may present a compelling opportunity to reassess portfolio positioning.

How Investors Can Position Fixed Income Portfolios

Rather than making concentrated bets, many strategists advocate a diversified approach.

A balanced portfolio may include:

Liquidity Allocation

Money market funds

Ultra-short duration funds

Cash reserves

Core Income Allocation

Intermediate-duration debt funds

Target maturity funds

Government securities

Tactical Allocation

Select long-duration opportunities

Duration positioning based on policy outlook

The objective is not simply maximizing yield.

The objective is maximizing risk-adjusted returns.

Conclusion

The growing institutional focus on the middle of the yield curve reflects a broader shift in how investors are approaching fixed income in 2026.

The 5-year segment offers a compelling combination of:

Positive carry

Roll-down benefit

Higher yields than short-term instruments

Lower volatility than long-duration bonds

For Indian investors navigating changing interest-rate expectations and evolving RBI policy, the middle of the curve may represent one of the most attractive opportunities in today’s debt markets.

Frequently Asked Questions

What is the middle of the yield curve?

The middle of the yield curve refers to bonds with maturities between five and seven years, often called the belly of the curve.

Why are investors buying 5-year bonds?

Many investors view 5-year bonds as offering an attractive balance between income generation, capital preservation, and duration risk.

What is positive carry?

Positive carry is the income earned by holding a bond, primarily through coupon payments and yield accrual.

What is a roll-down benefit?

Roll-down occurs when a bond moves closer to maturity and benefits from the lower yields associated with shorter-duration securities.

Are intermediate-duration bonds safer than long-term bonds?

Generally, they experience lower price volatility and reduced interest-rate sensitivity compared with long-term bonds.

How can Indian investors gain exposure to this strategy?

Through target maturity funds, debt mutual funds, government securities, corporate bonds, and professionally managed fixed income portfolios.

Introduction

Instead of asking whether bonds or equities are better, HNIs should be asking a different question:

How should each asset class contribute to my overall wealth strategy?

The most successful portfolios are rarely built around a single investment idea. They combine growth assets that create wealth with defensive assets that help protect it.

In 2026, that balance has become increasingly important.

Bond yields remain attractive relative to recent years, while equities continue to offer long-term participation in economic growth. As a result, many high-net-worth investors are reassessing how much capital should be allocated to each asset class.

The answer is not universal. It depends on your objectives, liquidity requirements, risk tolerance, investment horizon, and existing sources of wealth.

For most investors, the goal is not choosing between bonds and equities. It is building a portfolio where both work together.

Why Asset Allocation Matters More Than Investment Selection

Many investors spend significant time identifying the next winning stock, fund, or investment theme.

Yet portfolio outcomes are often driven more by asset allocation than by individual security selection.

For HNIs, a well-structured allocation framework helps:

Manage portfolio risk

Generate reliable income

Maintain liquidity for future opportunities

Participate in long-term wealth creation

Reduce the impact of market volatility

The objective is not to maximize returns at all costs. The objective is to achieve returns that are consistent with your financial goals.

What HNIs Are Allocating Today

There is no standard formula for every investor, but most portfolios typically fall within three broad allocation ranges.

Investor Type

Bonds & Fixed Income

Equities

Conservative

70–80%

20–30%

Balanced

40–60%

40–60%

Growth-Oriented

20–40%

60–80%

These ranges should be viewed as guidelines rather than rules.

A retired entrepreneur seeking income may require a very different portfolio from a business owner still focused on long-term capital growth.

The Role of Bonds in an HNI Portfolio

Bonds serve a purpose that goes far beyond generating interest income.

Stability During Market Volatility

Fixed-income investments typically experience lower price fluctuations than equities, helping reduce overall portfolio volatility.

Predictable Cash Flow

Coupon payments can provide a steady income stream without requiring investors to liquidate growth assets during unfavorable market conditions.

Portfolio Flexibility

Fixed-income holdings can also provide liquidity that allows investors to rebalance portfolios and take advantage of opportunities when markets become dislocated.

For investors who have already accumulated significant wealth, bonds often play an important role in preserving financial flexibility.

Why Equities Continue to Drive Long-Term Wealth Creation

While bonds provide stability, equities remain one of the most effective tools for long-term capital appreciation.

Participation in Economic Growth

Equity investors benefit directly from rising corporate earnings, innovation, and economic expansion.

Inflation Protection

Over long periods, equities have historically provided stronger protection against inflation than most fixed-income assets.

Compounding Returns

Reinvested earnings and long-term capital appreciation can significantly increase wealth over multi-decade investment horizons.

The trade-off is higher short-term volatility.

However, investors with sufficient time horizons are often rewarded for accepting that volatility.

A Practical Allocation Framework

The right portfolio depends not only on financial assets but also on the broader picture of an investor’s wealth.

Investor A

Age: 62

Recently exited a business

Requires ongoing income

Prioritizes capital stability

Potential allocation:

70% Bonds / 30% Equities

Investor B

Age: 42

Owns a growing business

Limited near-term liquidity needs

Focused on wealth accumulation

Potential allocation:

30% Bonds / 70% Equities

Both investors may have similar net worth, yet require entirely different portfolio structures.

This illustrates why allocation decisions should always reflect individual circumstances rather than generic market views.

Key Factors That Should Influence Allocation Decisions

Time Horizon

Investors with longer horizons can generally tolerate greater equity exposure.

Liquidity Requirements

Upcoming expenses, business investments, property purchases, or retirement withdrawals may justify larger fixed-income allocations.

Existing Wealth Concentration

Business owners and real estate investors often already have significant exposure to growth-oriented assets. Fixed income can provide diversification.

Market Environment

While investors should avoid attempting to time markets, periods of attractive bond yields may increase the relative appeal of fixed-income investments.

Common Mistakes HNIs Make

Even experienced investors can undermine long-term outcomes through poor allocation decisions.

Common mistakes include:

Holding excessive cash for prolonged periods

Becoming overexposed to a single asset class

Ignoring concentration risk in private businesses

Failing to rebalance after strong market moves

Chasing recent performance trends

Avoiding these mistakes often has a greater impact than identifying the next investment opportunity.

Why Rebalancing Matters

Portfolio construction is not a one-time exercise.

Over time, market movements can cause allocations to drift significantly from their intended targets.

For example, a portfolio initially allocated 60% equities and 40% bonds may become 75% equities and 25% bonds after a prolonged equity rally.

Without rebalancing, risk levels can increase unintentionally.

Many advisors recommend:

Quarterly portfolio reviews

Annual strategic rebalancing

Additional reviews following major life or liquidity events

A disciplined rebalancing process helps maintain alignment with long-term objectives.

Final Thoughts

There is no universally correct bond-to-equity allocation.

The most effective portfolios are built around investor objectives, not market predictions.

For many HNIs, bonds provide stability, income, and flexibility, while equities drive long-term growth.

The optimal strategy is rarely choosing one over the other.

It is combining both in a way that supports your financial goals, adapts to changing circumstances, and remains resilient across market cycles.

Frequently Asked Questions

How much should an HNI allocate to bonds?

Conservative investors may allocate 60–80% to fixed income, while growth-oriented investors may allocate 20–40%. The appropriate allocation depends on individual circumstances.

Are bonds better than equities?

Neither asset class is inherently superior. Bonds provide stability and income, while equities offer long-term growth. Most HNIs benefit from exposure to both.

How often should a portfolio be reviewed?

Quarterly reviews and annual rebalancing are common practices, with additional reviews following major life or liquidity events.

What is the ideal HNI portfolio mix?

There is no universal formula. The ideal allocation depends on risk tolerance, investment horizon, liquidity needs, and existing assets.

Global markets can react sharply to events such as U.S. Federal Reserve decisions, geopolitical tensions, inflation surprises, or currency fluctuations. Equity markets often experience immediate swings as investors reassess growth expectations and risk.

In contrast, Indian debt markets have historically been less reactive to periods of global volatility. While they are not immune to global events, domestic factors such as RBI policy, liquidity conditions, inflation expectations, and strong local investor demand often play a much larger role in determining bond yields in India.

Takeaway: India’s bond market is anchored by domestic demand and RBI policy, making it less sensitive to global shocks than many investors assume.

1. How Global Volatility Affects Debt Markets

Before understanding why India behaves differently, it’s important to understand how bond markets typically react to global events.

Debt markets are influenced by:

Interest rate movements

Inflation expectations

Currency fluctuations

Credit risk

Capital flows

When investors expect higher interest rates or inflation, bond yields generally rise and bond prices fall. However, the speed and magnitude of these reactions depend on the structure of each country’s bond market.

Unlike equities, which are heavily driven by sentiment and future earnings expectations, bonds are primarily valued based on expected cash flows and interest rates.

2. Six Reasons Indian Debt Markets Are Less Reactive

1. Strong Domestic Investor Base

India’s bond market is dominated by domestic institutions, including:

Banks

Insurance companies

Pension funds

Provident funds

Mutual funds

These investors typically allocate capital based on long-term liabilities rather than short-term market sentiment.

Over 70% of Government Securities are held by domestic institutions like banks, insurers, and provident funds, making foreign flows a secondary driver.

2. Deep Government Securities Market

Government securities (G-Secs) form the foundation of theIndian fixed income market.

Because they are backed by the Government of India, they are considered among the safest debt instruments available.

Regular primary auctions and strong institutional participation help maintain liquidity and market depth even during uncertain periods.

3. Lower Dependence on Foreign Capital

Compared with many emerging markets, India’s debt market relies less on foreign funding.

While foreign portfolio flows can influence yields, domestic institutions remain the dominant participants.

This reduces the risk of sharp yield spikes caused by sudden foreign capital outflows.

4. RBI Policy Has a Bigger Influence Than Global Events

For Indian bonds, the Reserve Bank of India often matters more than overseas market developments.

The RBI influences:

Repo rates (Current repo rate: 5.50% as of mid-2025)

System liquidity

Government bond demand

Inflation expectations

Tools such as Open Market Operations (OMO), Variable Rate Reverse Repo (VRRR), and liquidity facilities allow the RBI to directly influence funding conditions and bond yields.

For example, when the RBI injects liquidity into the banking system via VRRR or OMOs, demand for government securities often improves, helping stabilise yields

5. Predictable Cash Flows Reduce Market Panic

Unlike equities, bonds provide predetermined coupon payments and principal repayment schedules.

Because investors can estimate expected returns more easily, they are less likely to react aggressively to short-term global headlines.

India’s corporate balance sheets have been deleveraged over the past 7- 8 years, reducing credit risk and default probability.

This structural strength makes the debt market more resilient to external shocks.

“Mehul Pandya, Managing Director and Group CEO at CareEdge Group, stated that Indian debt market resilience is due to deleveraged corporate balance sheets, even as external shocks and global geopolitical uncertainties continue.”

This is a critical structural factor that reduces default risk and supports market stability.

3. A Recent Example of Market Resilience

One reason investors often view the debt market in India as relatively resilient is that domestic factors frequently outweigh global noise.

For example, in 2024–2025, despite global rate volatility and U.S. Treasury yield fluctuations, Indian government bond yields remained relatively stable due to strong domestic liquidity and the RBI’s calibrated stance on interest rates and inflation.”

This does not eliminate volatility, but it often reduces the magnitude of market reactions.

4. When Global Shocks Do Affect Indian Debt Markets

Indian debt markets are not completely insulated.

Investors should pay attention to four key risks:

1. U.S. Federal Reserve Rate Shocks

Aggressive rate hikes can increase global yields and affect capital flows into emerging markets.

2. Sharp Rupee Depreciation

A weaker rupee can raise imported inflation and influence future RBI decisions.

3. Large Foreign Investor Outflows

Although foreign ownership is relatively limited, significant outflows can still affect liquidity and yields.

4. Commodity Price Spikes

Higher crude oil prices can increase inflation expectations and put upward pressure on bond yields.

5. What Investors Can Do

Understanding how Indian debt markets behave can help investors make better asset allocation decisions.

1. Use G-Secs for Portfolio Stability

Government securities can help reduce overall portfolio volatility during uncertain periods.

2. Consider Laddering Bond Maturities

Holding bonds with different maturities can help manage interest rate risk.

3. Monitor RBI Policy Closely

Changes in RBI policy often have a larger impact on bond yields than global headlines.

4. Watch Inflation Trends

Inflation remains one of the most important drivers of fixed income returns.

5. Use Shorter Duration During Tightening Cycles

When interest rates are expected to rise, shorter-duration debt funds may help reduce sensitivity to yield movements.

6. Diversify Across Fixed Income Segments

Combining government bonds, high-quality corporate bonds, and debt mutual funds can improve portfolio resilience.

Conclusion

The relative resilience of Indian debt markets is not accidental. It is supported by a large domestic investor base, a deep government securities market, active RBI policy management, and stable domestic liquidity conditions.

While global volatility can influence bond yields in India through interest rates, foreign portfolio flows, commodity prices, and currency movements, domestic factors often remain the primary drivers of market behaviour.

For investors seeking stability, income, and diversification, understanding the structure of Indian debt markets can help build more balanced portfolios and make better long-term investment decisions.

Understanding fixed income can help investors build more stable portfolios and navigate uncertainty with greater confidence.

FAQs

Why are Indian debt markets less volatile than equities?

Because bond prices are driven primarily by interest rates, liquidity, and cash flows rather than investor sentiment and earnings expectations.

Does RBI policy affect bond yields?

Yes. RBI decisions on rates and liquidity are among the most important drivers of bond yields in India.

Can global events impact Indian bonds?

Yes. Federal Reserve decisions, commodity prices, currency movements, and foreign capital flows can influence bond markets.

Are government securities safer than corporate bonds?

Generally yes, because they are backed by the Government of India and carry lower credit risk.

Can fixed income investments improve portfolio stability?

Yes. Fixed income investments can provide diversification, regular income, and lower volatility compared to equities.

Usually, when the RBI cuts rates, bond yields also fall. But this time, yields are still moving up.

This makes the current Indian debt market 2026 important for anyone with fixed deposits (FDs), debt mutual funds, or anyone planning to take a loan. In this article, you’ll understand why yields are rising, what it means for different investors, and five practical steps you can take to make better investment decisions.

Metric

Value (June 2026)

10-year G-sec yield

6.95% – 7.10%

RBI repo rate

5.25% (-100 bps this year)

US 10-year Treasury yield

4.30% – 4.60%

India-US yield spread

1.6% – 2.0%

91-day T-Bill

5.30% – 5.60%

30-year G-sec

7.40% – 7.70%

Average Bank FD

6.5% – 7.1%

These numbers show an interesting situation: while the RBI has reduced rates, market bond yields are still higher because of global market conditions and supply-related factors.

Why Are Bond Yields Rising Despite RBI Rate Cuts?

Global Factors: US Yields and Foreign Investor Activity

US bond yields continued rising in early 2026, taking the US 10-year Treasury yield to around 4.59%. This reduced the gap between Indian and US bond yields to around 1.8%, which is much lower than usual.

When this gap becomes smaller, foreign investors may find Indian bonds less attractive. The continued reduction in spread gap since the begining of the calendar yearThis contributed to foreign debt outflows of $12.6 billion in between Jan-Mar’26Q4 FY26, along with larger outflows between May 2025 and May 2026, putting upward pressure on Indian bond yields.

Domestic Factors: Government Borrowing and Fiscal Concerns

Investors are also watching government borrowing closely.

India is expected to have a fiscal deficit of around 4.2% in FY27, which means the government may need to borrow more money.

When more bonds are issued into the market, supply increases. If demand does not rise at the same pace, bond prices can fall and yields can move higher.

Inflation, Oil Prices, and Global Risks

Rising oil prices and global tensions are also creating concerns about inflation.

Higher oil prices can increase transportation and business costs, which may push inflation higher. Because of this, investors demand higher returns from long-term bonds, keeping yields elevated even when short-term interest rates are reduced.

Current Yield Snapshot (June 2026)

Investment Type

Yield

Current Trend

91-day T-Bill

5.34 %

Stable in the short term

10-year G-sec

6.99%-7.10%

Up by 0.35% this year

30-year G-sec

7.63%-7.67%

Higher returns for longer periods

US 10-year Treasury

4.46% to 4.50%

Gap with India is narrowing

Average Bank FD

6.5–7.1%

Lower than G-sec yields

Note: A 35 basis point increase simply means yields increased by 0.35%, which is a noticeable movement for investors looking for stable income and capital protection.

What Does This Mean for Different Investors?

Retail Investors (₹10–50 Lakhs)

Opportunity: Mid-to-long-term government bonds are offering around 7.40% returns, which is slightly higher than average FD rates of 6.5–7.1%.

Possible strategy:

Spread investments across different periods instead of investing all at once

Consider 5-7 year investments for a balance between returns and risk

Dynamic bond funds can help adjust to changing market conditions

Things to keep in mind:

Government bonds are generally low-risk, but taxes and liquidity needs can affect your final returns.

High Net Worth Individuals (₹50 Lakhs+)

Opportunity:

HNIs can diversify into government bonds and other high-quality debt products for better returns while maintaining liquidity.

Possible strategy:

Mix gilt funds and quality debt products

Spread investments across different maturity periods

Use customized investment strategies where required

Borrowers (Home Loans or Business Loans)

What this means:

Loan EMIs may remain high if bond yields continue rising.

Possible actions:

Compare fixed and floating rates before borrowing

Consider fixed rates for larger loans

Prepay loans with interest above 9% if possible

Equity Investors

What this means:

Higher bond yields can increase costs for companies and affect stock performance.

Sectors that may feel pressure include:

Real estate

NBFCs

Technology companies

Companies with lower debt and stronger cash flow may perform better.

5 Simple Action Steps

Review your current allocation between FDs, bonds, and debt funds

Consider 5–7 year government bond exposure if retirement is still 5–10 years away

Add some allocation to dynamic bond funds

Compare fixed-rate loan options and reduce debt with interest above 9%

Watch the RBI June 2026 meeting, US interest rates, and oil prices

FDs vs G-Secs vs Bond Funds: Quick Comparison

Investment Type

Current Yield (May 2026)

Liquidity

Main Risk

Fixed Deposits (FDs)

3.05% to 6.45%

Medium

Inflation may reduce real returns

Government Securities (G-Secs)

6.99% to 7.00%

Medium

Prices can change with interest rates

Dynamic Bond Funds

Varies

High

Fund performance depends on market movements and fund decisions

What Could Happen in 2026?

If things improve (around 6.5%)

If inflation falls and oil prices stay below $85, bond yields may gradually come down.

If things remain stable (6.5-7.0%)

If the economy continues performing normally, bond yields may stay within the current range with some market ups and downs.

If risks increase (above 7.2%)

If government spending concerns increase or oil prices move above $95, bond yields could rise further.

The main factors to watch are:

RBI policy decisions

US interest rates

Oil prices

Why Mid-2026 Could Be Important for Indian Bonds

India is expected to be included in the Bloomberg Global Aggregate Index in mid-2026.

This could bring around $25 billion of foreign investment into Indian bonds.

More investment demand may help reduce yields over time. However, the exact timing and impact are still uncertain.

Frequently Asked Questions

Q1: Is this a good time to invest in bond funds?

Current 10-year yields of 7.03% may create attractive opportunities for investors looking for regular income. Dynamic bond funds can also help manage changing interest rates.

Q2: Are G-Secs better than FDs in 2026?

Government securities are currently offering around 7.40%, which is slightly higher than average FD rates of 6.5–7.1%. However, taxes and price movements should also be considered.

Q3: Why are yields rising even after RBI reduced rates?

Main reasons include:

Higher global yields

Foreign investors reducing investments

More government borrowing

Inflation concerns

Q4: Should I move to long-term bond funds?

Long-duration funds may work better for investors with a longer investment horizon and comfort with short-term market fluctuations. Others may prefer dynamic or medium-duration funds.

Conclusion

The Indian debt market in 2026 is creating both opportunities and challenges for investors.

With the 10-year G-sec yield at 7.03%, around 7.00%, investors may find attractive income opportunities. But instead of chasing higher returns, focus on diversification, investment time horizon, and regular portfolio reviews.

Many investors treat debt and fixed income as the “stable” part of a portfolio and rarely revisit it after allocation. That approach can become expensive over time.

A well-designed fixed income allocation is not static. It should evolve as market cycles change. Interest rates move, inflation expectations shift, liquidity conditions tighten or improve, and credit risks emerge in different phases of the economy.

The same fixed income product can perform very differently depending on where markets stand in the cycle. A long-duration bond fund may struggle during rising-rate environments but perform strongly when rates begin to decline. A lower-rated bond offering attractive yields may look compelling during stable periods but become risky during economic stress.

Successful fixed income investing is not about constantly chasing returns. It is about managing three important levers:

Duration

Credit quality

Liquidity

Understanding how these factors interact can help investors build a stronger fixed income portfolio that adapts to changing market conditions.

Why Market Cycles Matter

Interest rates, inflation, and credit conditions influence the performance of debt products.

When inflation rises, central banks often increase interest rates to slow economic activity. Higher rates can pressure existing bond prices.

When inflation begins to ease, rate cuts may follow, creating opportunities in longer-duration assets.

Credit conditions also shift with economic cycles. During stable periods, investors may become comfortable taking additional credit risk. During uncertain periods, safety and liquidity often become more important.

This explains why the same debt product behaves differently across cycles.

For example:

Long-duration government securities may benefit from falling rates.

Short-duration instruments may protect capital during rising rates.

Lower-credit instruments may offer higher income but can become vulnerable during economic stress.

Understanding bond allocation by market cycle allows investors to make allocation decisions based on market environments rather than assumptions.

The 3 Core Levers of Fixed Income Allocation

1. Duration

Duration measures how sensitive a bond or debt instrument is to interest-rate changes.

Higher duration:

More sensitive to interest rates

Higher potential gains if rates fall

Higher potential losses if rates rise

Lower duration:

Lower interest-rate sensitivity

More stable during volatile rate environments

A strong duration strategy becomes particularly important when rates are changing rapidly.

2. Credit Quality

Credit quality reflects the issuer’s ability to repay debt obligations.

Higher credit quality:

Lower default risk

Lower yield potential

More stability

Lower credit quality:

Higher yields

Higher risk

Understanding credit quality in fixed income helps investors avoid confusing higher yields with safer returns.

3. Liquidity

Liquidity refers to how easily an investment can be converted into cash without affecting value significantly.

Higher liquidity matters because it:

Supports emergency needs

Reduces forced selling risk

Adds flexibility during uncertain periods

Liquidity becomes especially important during market stress.

How to Adjust Fixed Income Allocation Across Cycles

Rising-Rate Cycle

In a rising-rate environment, new bonds are issued at higher yields, making older bonds less attractive.

Recommended approach:

Focus on shorter-duration products

Prioritize high credit quality

Maintain liquidity

Potential allocation preference:

Short-term debt funds

Treasury bills

Corporate bonds with shorter maturity

Avoid taking excessive duration exposure during this phase.

Peaking-Rate Cycle

This phase occurs when interest rates appear close to their highest point and policy tightening slows.

Recommended approach:

Gradually extend duration

Maintain quality exposure

Begin positioning for future opportunities

Potential allocation preference:

Medium-duration bond funds

Government securities

High-quality corporate debt

This phase often creates opportunities before markets fully price in future rate changes.

Falling-Rate Cycle

Falling-rate environments can benefit longer-duration instruments.

Recommended approach:

Increase duration exposure

Lock in attractive yields

Continue balancing quality

Potential allocation preference:

Long-duration funds

Government bond exposure

High-quality fixed-income securities

Long-duration assets generally benefit more when rates decline.

Volatile or Uncertain Cycle

Periods of uncertainty require a balanced approach.

Recommended approach:

Maintain flexibility

Focus on liquidity

Reduce unnecessary credit risk

Potential allocation preference:

Money market funds

Short-duration products

High-quality bonds

Capital preservation often becomes more important than maximizing returns.

Fixed Income Allocation by Market Cycle: Quick Comparison

Market Phase

Duration Preference

Credit Quality

Liquidity Focus

Rising rates

Short

High

Moderate

Peaking rates

Medium

High

Moderate

Falling rates

Long

High to moderate

Lower

Volatile markets

Short to medium

Very high

High

For example, if an investor has ₹10 lakh in fixed income, the mix can change depending on market conditions. When interest rates are rising, more money may go into liquid funds or short-term debt products. When rates are near their peak, some amount can move into medium-term bonds. When rates start falling, investors may increase long-term bond exposure to benefit from potential gains. During uncertain markets, the priority usually shifts back to safer and more liquid investments.

A Practical Bucket Framework for Debt Allocation

Instead of allocating fixed income based only on products, allocate based on purpose.

Near-Term Cash Needs

Objective:

Capital protection and immediate access.

Examples:

Emergency funds

Upcoming expenses

Short-term goals

Possible exposure:

Liquid funds

Money market instruments

Fixed deposits

Medium-Term Stability

Objective:

Reduce volatility while earning reasonable returns.

Examples:

Education planning

Planned purchases

Portfolio stability

Possible exposure:

Corporate bond funds

Short to medium-duration products

Opportunistic Income

Objective:

Capture opportunities arising from market conditions.

Examples:

Tactical positioning

Rate-cycle opportunities

Possible exposure:

Dynamic bond funds

Long-duration funds

Select credit opportunities

This debt allocation strategy creates flexibility while keeping goals at the center of decisions.

Common Mistakes Investors Make

Chasing Yield

Higher yields can be attractive, but they often come with higher risks.

A 10% yield is not automatically better than a 7% yield if the additional risk is substantial.

Ignoring Duration Risk

Many investors focus only on returns and overlook duration.

Interest-rate sensitivity can significantly affect portfolio performance.

Overlooking Liquidity

Investments that appear attractive on paper can become difficult to exit during stress periods.

Liquidity should always be considered.

Treating All Debt Products the Same

Fixed deposits, government securities, debt mutual funds, and corporate bonds behave differently.

Each serves a different role within a fixed income portfolio.

Rebalancing Rule: How Often Should You Review Fixed Income Allocation?

Investors often review equity exposure more frequently than debt allocation.

That creates imbalance.

A practical approach is:

Quarterly reviews for active investors

Every six month reviews for most retail investors

Additional reviews after major interest-rate changes

When deciding how to rebalance debt portfolio exposure, focus on:

Financial goals

Time horizon

Rate outlook

Risk tolerance

Liquidity requirements

Rebalancing should be driven by portfolio needs rather than market headlines.

Conclusion

A successful fixed income allocation is not built around finding the highest yield.

It is built around maintaining the right balance between duration, credit quality, and liquidity.

Market cycles change continuously, and debt portfolios should adapt accordingly. Investors who align allocation with the cycle often improve portfolio resilience while avoiding unnecessary risk.

The goal of fixed income investing is not simply generating returns. It is creating a portfolio that remains aligned with changing market realities and long-term objectives.

Frequently Asked Questions

What is fixed income allocation?

Fixed income allocation refers to the portion of a portfolio invested in debt instruments such as bonds, fixed deposits, government securities, and debt funds. It helps provide income, stability, and diversification.

How should debt allocation change when rates rise?

During rising-rate environments, investors typically reduce duration exposure and focus on shorter-term, higher-quality debt instruments.

Is duration more important than yield?

Duration and yield serve different purposes, but duration becomes critical when interest rates are changing significantly because it affects price sensitivity and portfolio volatility.

How often should investors rebalance fixed income?

Most investors should review and rebalance fixed income exposure every six months, while active investors may review quarterly.

What is the safest fixed income strategy in volatile markets?

During volatile environments, investors generally prioritize high credit quality, shorter duration, and greater liquidity.

How does fixed income investing work in India?

Fixed income investing in India includes products such as government securities, corporate bonds, debt mutual funds, treasury bills, and fixed deposits. Performance depends on interest rates, credit conditions, and market cycles.

Why Are Bond Yields Still Volatile Despite RBI’s Liquidity Push?

If the RBI has been injecting liquidity into the financial system, why are bond yields still moving unpredictably?

The answer is straightforward: RBI liquidity actions influence the debt market, but they are not the only force driving yields. Government borrowing, currency risk, inflation expectations, global oil prices, foreign capital movement, and market sentiment continue shaping the direction of India’s bond market.

For investors searching for terms like RBI liquidity impact on Indian debt market 2026, understanding this relationship matters because it directly affects:

Bond fund performance

Government securities (G-Secs)

Corporate bond returns

Fixed income portfolio strategy

HNI wealth allocation decisions

In 2026, the RBI has been balancing:

Approximately ₹30 trillion debt supply pressure

State borrowing requirements

Banking system deposit gaps

Rupee defense measures

Foreign exchange outflows

Geopolitical and Middle East risks

RBI Liquidity Actions and Their Impact

RBI Tool

Effect on Bonds

2026 Example

Open Market Operations (OMO)

Adds liquidity and generally reduces yields

₹2.15L Cr liquidity plan

Forex Swaps

Adds rupee liquidity

$10B USD-INR swap (Feb 4, 2026)

CRR Reduction

Frees banking liquidity

Banking liquidity support

Liquidity Drain

Removes excess cash and can raise yields

Inflation control measures

Definition: RBI liquidity actions are central bank measures used to inject or absorb money from the financial system to influence borrowing costs and market liquidity.

RBI’s Liquidity Toolkit: How the Central Bank Influences Bond Yields

Why Are Yields Still Volatile Despite RBI Support?

Liquidity injections usually soften yields, but they cannot eliminate volatility.

The 10-year G-Sec yield remained around 7.03–7.05% during mid-May 2026, showing that markets continue reacting to broader risks.

Key factors include:

Large government borrowing programs

Rising crude oil prices

Middle East geopolitical uncertainty

Significant deprecitation of Indian rupee agains USD

Foreign capital outflows

Inflation expectations

This reinforces an important takeaway: RBI liquidity actions influence the Indian debt market, but they do not completely override supply and macroeconomic forces.

Portfolio Implications for Retail and HNI Investors

Opportunities

1. Short-duration debt strategies

Current conditions may favor:

Short-term debt funds

Banking and PSU funds

High-quality corporate debt

Target maturity funds

2. Improved sentiment environment

Cooling inflation alongside liquidity support may improve:

Fixed income demand

Portfolio stability

Income opportunities

3. Attractive HNI positioning opportunities

Investors can consider:

Bond ladder strategies

Diversified debt allocation

Duration balancing

Risks Investors Should Monitor

Large debt supply

Global volatility

Inflation surprises

Liquidity withdrawal risks

FAQ

How do RBI OMOs affect my bond fund?

OMOs generally support bond prices and may benefit debt fund valuations.

Why do bond yields fall after liquidity injections?

Additional liquidity increases bond demand, which raises prices and lowers yields.

Are short-duration funds attractive in 2026?

They may offer lower interest-rate sensitivity during periods of uncertainty.

How do forex swaps affect debt markets?

Forex swaps inject rupee liquidity into the financial system and ease funding conditions.

What is the outlook for Indian bond markets in 2026?

Liquidity support remains positive, but borrowing pressures and global risks could keep volatility elevated.

Why Many Investors Are Moving Beyond Fixed Deposits

Imagine this.

You have ₹10 lakh parked in fixed deposits earning 6-6.5% annually. It feels safe. But with inflation hovering around 4-5%, your real return barely grows your wealth.

Now consider this: Government securities in India are currently yielding around 6.8-7.2%. High-quality corporate bonds can offer 7.5-8.5%, and select structured bonds may offer even more.

So the real question becomes:

Why rely on just one fixed income instrument when a simple diversification strategy could increase yields while maintaining safety?

Many retail and HNI investors assume that diversifying bonds requires complex strategies or institutional expertise. With a few practical steps, investors can build a stable, diversified fixed-income portfolio that balances safety, liquidity, and yield.

Why Diversification Matters in Fixed Income Investing

Most investors diversify equities but forget that fixed income also carries risks.

Holding only one type of instrument like FDs or a single corporate bond, exposes investors to unnecessary concentration risk.

A diversified fixed income portfolio helps:

Improve yield potential

Reduce credit risk

Manage interest rate fluctuations

Maintain liquidity

Generate predictable income

For example, instead of putting ₹10 lakh entirely in one FD, an investor could spread investments across government securities, corporate bonds, SDLs, and inflation-protected instruments.

This approach increases stability while improving returns.

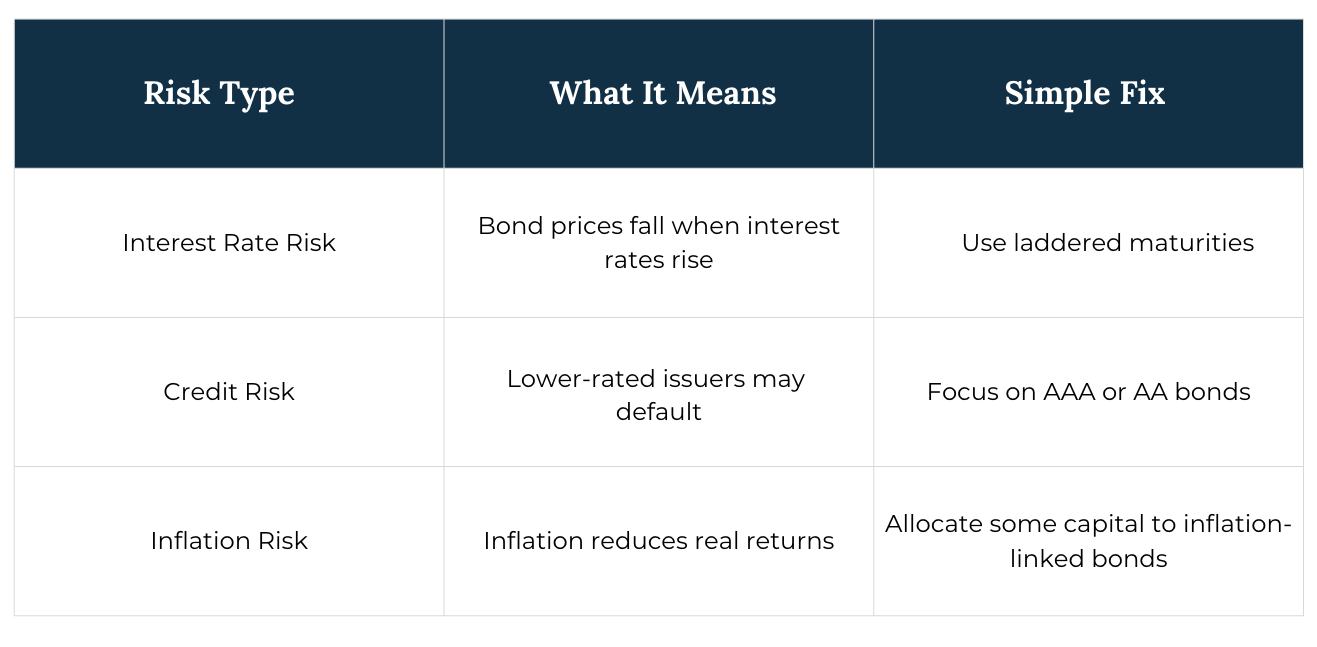

Key Risks in Fixed Income Investing (And How to Manage Them)

Even safe investments carry risks. The goal is risk management through diversification.

A balanced portfolio reduces the impact of these risks.

Simple Strategies to Diversify Fixed Income Investments

Investors do not need complicated financial engineering to diversify bonds. A few proven strategies work well.

1. Bond Laddering (Best for Stability)

Bond laddering means buying bonds with staggered maturities.

Example allocation:

Benefits:

Provides regular liquidity

Reduces interest rate risk

Allows reinvestment when rates change

Investors can easily build ladders using Government Securities (G-Secs) through the RBI Retail Direct platform.

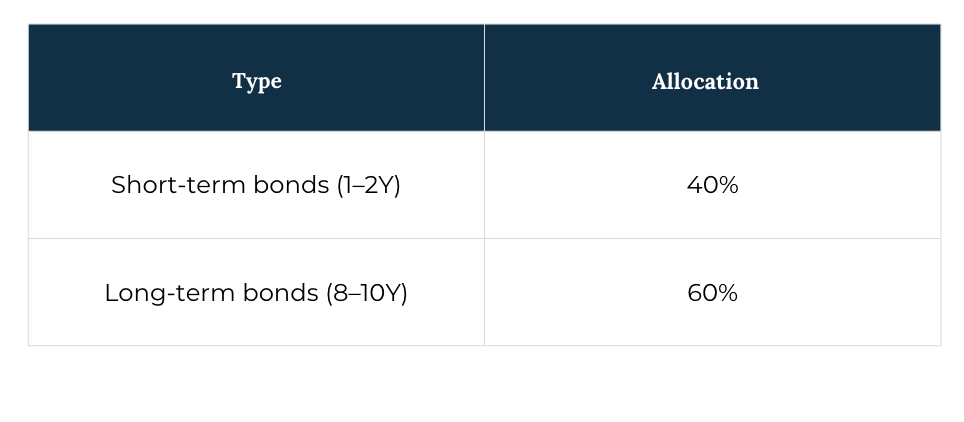

2. Barbell Strategy (Balancing Yield & Liquidity)

Another simple approach is the barbell strategy, where investors combine:

Short-term bonds (for liquidity)

Long-term bonds (for higher yield)

Example:

This approach balances cash flow stability with higher returns.

3. Mix Different Fixed Income Instruments

Instead of relying on one type of bond, investors should diversify across instruments.

Example portfolio structure:

This mix combines sovereign safety with yield enhancement.

Fixed Income Opportunities in 2026

The Indian fixed income market currently offers interesting opportunities.

1. Stable RBI Interest Rate Outlook

The RBI has maintained a neutral stance on rates, while inflation has gradually moderated. This environment supports stable bond yields.

2. Attractive State Development Loans (SDLs)

SDLs often provide 30–60 basis points higher yield than G-Secs with relatively low risk.

3. Growth of Green Bonds

India’s sustainable finance market is expanding, and green bonds issued by government-backed institutions are becoming attractive for long-term investors.

4. Tax Efficiency

Long-term bond investments may benefit from favorable tax treatment depending on holding structure and investment vehicle.

Investors should evaluate tax implications carefully when structuring fixed income portfolios.

Platforms Where You Can Buy Bonds in India

Today, investing in bonds is far easier than it used to be.

Retail investors can access diversified fixed-income investments through platforms such as:

RBI Retail Direct

Allows investors to buy government securities directly from RBI auctions.

NSE goBID

Enables participation in government bond auctions via stock exchanges.

Online Bond Platforms

There are multiple Online bond Pplatforms which such as GoldenPi allow investors to explore corporate bonds and structured fixed-income products.

Investment Apps

Debt mutual funds and bond ETFs are also accessible through apps like Groww or Zerodha.

Typical process:

Open an account on a platform

Browse available bonds

Evaluate yield and credit rating

Build a diversified basket

Minimum investment for many bonds starts from ₹10,000.

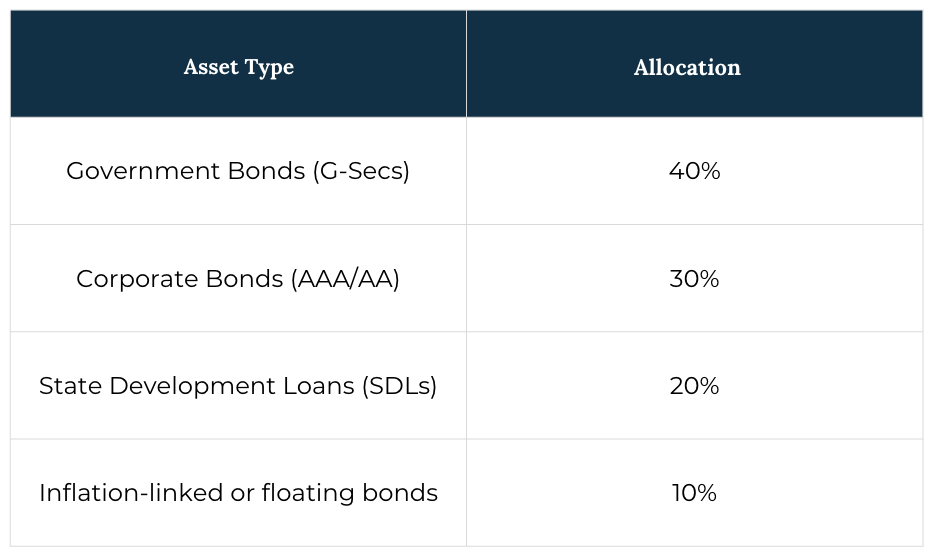

Example Fixed Income Portfolio (₹10 Lakh)

Here is a simple diversified allocation for an investor seeking stability and yield.

Expected portfolio yield: 7.5-8% with moderate risk

Compared to traditional FDs, this strategy could add 1-2% additional yield annually.

Frequently Asked Questions

What is the minimum investment required for bonds in India?

Many bonds are available from ₹10,000 onwards, though some corporate bonds may require higher minimums.

How often should a fixed income portfolio be rebalanced?

A yearly review is sufficient for most investors.

Are debt mutual funds better than direct bonds?

Debt funds are suitable for investors seeking professional management and diversification, while direct bonds provide greater control over yields and maturities.

Are corporate bonds safe?

High-quality AAA and AA-rated bonds from strong issuers generally offer a good balance of safety and yield.

Final Thoughts

Fixed income investing does not have to be complicated.

By combining government bonds, corporate bonds, SDLs, and inflation-linked instruments, investors can build a diversified portfolio that delivers:

Stable income

Higher yield than traditional FDs

Lower risk through diversification

For both retail and HNI investors, the key is to keep the strategy simple, disciplined, and diversified.

Even starting with ₹1 lakh can help investors begin building a well-balanced fixed income portfolio.

In today’s interconnected financial world, the impact of central bank announcements are much faster than it was earlier due to technological advancements, no longer just technical policy updates. Their statements, meeting minutes, and press releases conferences play a major role in shaping bond markets around the world. Understanding these signals is not only important for large institutional investors but also for. It has become increasingly relevant for everyday investors as well.

If you invest in debt mutual funds, government bonds, fixed deposits linked to market rates, or other fixed-income instruments, central bank decisions can directly influence the returns and risks of your investments.

Simply put, learning how to interpret central bank signals is becoming an essential skill for anyone investing in fixed income.

This guide breaks down everything you need to know: which announcements of central banks matter most, what signals they send, how those signals move bond yields, what current conditions indicate, and most importantly how you can position your fixed-income portfolio intelligently.

1. Understanding Central Bank Signals in Fixed Income Markets

At its core, the price of a bond is determined by interest rates. When rates rise, existing bond prices fall. When rates fall, bond prices rise. This inverse relationship is fundamental to fixed-income investing. But what causes interest rates to move? In large part, it is the decisions and the anticipated decisions of central banks.

Central banks do not simply change rates overnight. They communicate well in advance through a range of signals: policy statements, forward guidance, voting records, dot plots, and governor speeches. Experienced investors parse every word of these communications because the market often moves on what is expected, not what has already happened.

Why This Matters for Retail Investors

If you hold a long-duration debt mutual fund and the RBI or Fed signals a prolonged rate hike cycle, your NAV could erode significantly before a single rate hike is officially announced. Understanding the signals lets you act before the market has fully priced them in.

For retail investors, the importance is threefold:

Return implications: Bond prices and yields move in anticipation of central bank action, not just after it.

Risk management: Knowing where rates are headed helps you manage duration risk and the sensitivity of your portfolio to rate changes.

Opportunity recognition: Rate cycles create predictable windows of opportunity in specific bond categories.

2. The Major Central Banks Driving Global Bond Markets

Not all central banks carry equal weight. While every country has its own monetary authority, a handful of institutions drive global capital flows and set the tone for bond markets worldwide.

The Fed is the most influential central bank in the world. Its decisions on the federal funds rate ripple through every major bond market. When the Fed raises rates, capital tends to flow towards U.S. Treasuries, causing yields in emerging markets (including India) to rise as well, as investors demand higher returns to compensate for the outflow risk. The Fed’s FOMC meets eight times a year, and its dot plot, a chart showing individual members’ rate expectations, is one of the most closely watched documents in global finance.

The ECB governs monetary policy for the 20-nation Eurozone. Its decisions directly affect European sovereign bond markets – German Bunds, French OATs, Italian BTPs and influence dollar-euro dynamics that affect cross-border bond flows globally. ECB President press conferences and the quarterly Staff Economic Projections are critical signal sources.

The Bank of England (BoE)

The UK Monetary Policy Committee meets roughly every six weeks and publishes detailed minutes and quarterly Monetary Policy Reports. Given the UK’s close financial ties with both Europe and emerging markets, BoE signals have a meaningful secondary effect on global risk appetite.

The Reserve Bank of India (RBI)

For Indian retail investors, the RBI is the central bank that matters most directly. The Monetary Policy Committee (MPC) meets six times a year and sets the repo rate – the key rate that influences everything from government bond yields to corporate fixed deposits. RBI Governor speeches, liquidity management operations, and the bi-monthly policy statement are all critical signal sources that retail investors should follow closely.

The Bank of Japan (BoJ)

Japan’s ultra-loose monetary policy for decades made it a major exporter of global capital through the so-called ‘carry trade.’ As the BoJ shifts away from Yield Curve Control (YCC), it is becoming an increasingly important signal source – any tightening from Tokyo sends ripples through Asian bond markets and global risk sentiment.

The People’s Bank of China (PBoC)

China’s role in global bond markets has grown substantially. The PBoC’s management of lending rates (LPR), reserve requirements, and currency policy has a direct bearing on Asian credit markets and commodity-linked economies, including India.

3. The Key Signals Investors Should Watch

Central banks communicate through multiple channels. Learning to read each one gives you a significant informational edge.

Policy Rate Decisions

The headline number, whether rates are hiked, cut, or held is the most obvious signal. But the magnitude matters too. A 25bps hike signals measured tightening; a 50bps or 75bps hike signals urgency and can cause sharp bond sell-offs.

Forward Guidance

Forward guidance is the explicit communication of where central banks expect rates to go. Phrases like ‘higher for longer,’ ‘data-dependent,’ or ‘accommodative stance’ carry enormous weight. When the Fed shifted from ‘transitory inflation’ language to signalling sustained rate hikes in 2022, long-duration bond portfolios suffered dramatic losses within months.

Dot Plots and Rate Projections (Fed-Specific)

The Fed’s dot plot shows each committee member’s anonymous projection for where the federal funds rate will be at year-end and over the next several years. A shift in the median dot upward is a hawkish signal; downward movement is dovish. Retail investors should review the dot plot after every FOMC meeting.

Hawkish vs. Dovish Language

Hawkish signals indicate a bias towards tighter monetary policy (higher rates). Dovish signals indicate a bias towards easier monetary policy (lower rates). Watch for language changes between consecutive meetings even removing a single phrase like ‘ongoing rate increases’ can be a significant dovish pivot.

Inflation and GDP Projections

When central banks revise their inflation forecasts upward, it signals that rates may need to stay elevated longer. When growth forecasts are cut, it often signals that rate cuts are approaching to stimulate the economy. Both scenarios have direct consequences for bond pricing.

Voting Records and Dissents

MPC and FOMC voting records reveal internal disagreement. A committee that was previously unanimous for hikes but shows one or two dissenting votes signals that the end of the tightening cycle may be near. This is one of the most underappreciated signals available to retail investors.

Balance Sheet Actions (QE / QT)

Quantitative Easing (QE) involves a central bank buying bonds, injecting liquidity and pushing yields down. Quantitative Tightening (QT) does the opposite, selling bonds or allowing them to mature, withdrawing liquidity and pushing yields up. These balance sheet decisions are as important as rate decisions for long-duration bond investors.

4. How Central Bank Signals Move Bond Yields

Understanding the transmission mechanism and how signals translate into yield movements is critical.

Short-End vs. Long-End Dynamics

Short-duration bonds (1-3 year) are most directly affected by current and near-term policy rate expectations. Long-duration bonds (10-30 year) are more sensitive to inflation expectations, growth outlook, and long-term rate projections. This is why the yield curve – a plot of yields across maturities is such a valuable diagnostic tool.

The Yield Curve as a Signal

A normal (upward-sloping) yield curve reflects healthy growth expectations. An inverted yield curve (short-term rates above long-term rates) has historically been one of the most reliable recession indicators. A flat curve often signals a transition period. Monitoring yield curve shape helps retail investors anticipate economic and rate cycle shifts before they are officially announced.

Duration Risk: The Most Misunderstood Concept

Duration measures a bond’s sensitivity to interest rate changes. A bond with a duration of 7 years will lose approximately 7% in price for every 1% rise in yields. Many retail investors in long-duration debt funds do not appreciate this risk until they experience it firsthand. In a rising rate environment, short-duration bonds significantly outperform long-duration ones.

Duration Risk Example

If you hold a debt mutual fund with an average duration of 8 years and yields rise by 100bps (1%), your fund NAV could decline by approximately 8%. This is why understanding central bank signals and positioning your duration accordingly is not optional for serious fixed-income investors.

Credit Spreads and Liquidity

Beyond government bonds, central bank signals affect corporate bond spreads as well. Hawkish signals tighten liquidity, widen credit spreads, and increase borrowing costs for corporates making corporate bonds riskier. Dovish signals compress spreads, improving returns on credit instruments.

5. What Current Global Signals Are Indicating

As of early 2026, major central banks have paused rate adjustments after prior cuts, balancing resilient growth (India GDP projected at 7.4%) with persistent inflation risks and global uncertainties. Retail investors should monitor upcoming MPC/FOMC meetings closely, as language shifts could signal restarts to easing or tightening.

The U.S. Federal Reserve

The Federal Reserve kept the federal funds rate unchanged at 3.5%-3.75% in March 2026, marking the second consecutive pause. The Fed’s projections currently indicate only one rate cut, as the labor market remains strong and services inflation is still elevated.

The Reserve Bank of India

The RBI has kept the repo rate steady at 5.25% since December 2025, with the neutral policy stance confirmed in the February 2026 MPC meeting. Although inflation has eased to 3.21% (February CPI YoY), the 10-year G-Sec yield has risen to around 7.0%, largely due to oil price shocks and higher state government borrowing.

The ECB and Bank of England

Both central banks are currently holding rates steady. The Bank of England maintained the Bank Rate at 3.75% on March 19, 2026, with a unanimous vote, as policymakers remain cautious due to persistent energy-related inflation. The ECB is also maintaining a cautious stance, balancing inflation concerns with slower economic growth.

The Bank of Japan: The Outlier

The Bank of Japan is gradually raising rates toward its 2% inflation target, reaffirmed in March 2026. These policy moves are also contributing to the unwinding of yen carry trades, which is adding some volatility to global markets.

6. Impact on Fixed Income Markets

Central bank signal divergence has created a complex but opportunity-rich environment across fixed income sub-segments.

Government Bonds: Easing cycles in India and the West are supportive of sovereign bond valuations. Indian G-Secs are particularly attractive given current yield levels relative to anticipated rate cuts.

Corporate Bonds and Credit: As liquidity conditions improve, investment-grade corporate spreads tend to compress, offering alpha over government bonds for investors willing to take measured credit risk.

Floating Rate Instruments: In environments of rate uncertainty, floating rate bonds and funds offer a hedge against unexpected tightening.

Emerging Market (EM) Debt: A dovish Fed typically weakens the dollar, providing support to EM currencies and making EM debt more attractive to global investors.

Short-Duration Instruments: Liquid funds, ultra-short bond funds, and short-term FDs continue to offer attractive real returns in the current environment, with minimal duration risk.

7. Opportunities Emerging in Fixed Income

The current pause in interest rates (as of April 2026) is creating selective opportunities for retail investors in fixed income. With India’s 10-year G-Sec yield around 7.0%, investors can benefit from relatively high yields, but should remain mindful of inflation risks and fiscal pressures. The focus should be on high-quality instruments and moderate duration, rather than assuming immediate rate cuts.

Locking in Elevated Yields

Interest rates remain higher than historical averages, with the RBI repo rate at 5.25% and the 10-year G-Sec yield around 7.0%. This provides attractive income potential for investors. Extending duration moderately into 3-7 year government bond funds can offer a balanced risk-return profile, but only if the investment horizon matches, especially as inflation remains in the 3-5% range.

Indian Government Securities (G-Secs)

India’s inclusion in the JP Morgan GBI-EM index continues to attract foreign investor inflows, estimated at $20–25 billion cumulatively by early 2026. This has helped support bond demand even as oil price shocks recently pushed yields up by around 30 basis points. For retail investors, gilt funds or target maturity funds are practical ways to access G-Secs. The current 10-year yield of about 7.0% remains attractive if global liquidity conditions remain supportive.

Target Maturity Funds

Target maturity funds offer a simple and structured way to invest in bonds. They provide predictable maturity timelines, tax efficiency, and potential market gains. If interest rates decline after the current pause, investors could benefit from regular accrual income along with potential capital gains of around 2-4% from falling yields. These funds are generally suitable for investment horizons of 3-7 years.

High-Quality Corporate Bonds